For two decades, property development powered China’s growth story. Urbanization, easy credit, and speculative buying created an unprecedented construction boom.

Major developers like:

- China Evergrande Group

- Country Garden

- Sunac China

expanded aggressively through high leverage, offshore dollar bonds, and pre-sale financing models.

The system worked — until it didn’t.

🚨 What Triggered the China Property Crash?

1️⃣ The “Three Red Lines” Policy (2020)

In 2020, Beijing introduced debt-control measures limiting borrowing for developers who crossed leverage thresholds.

This instantly squeezed liquidity for highly indebted builders.

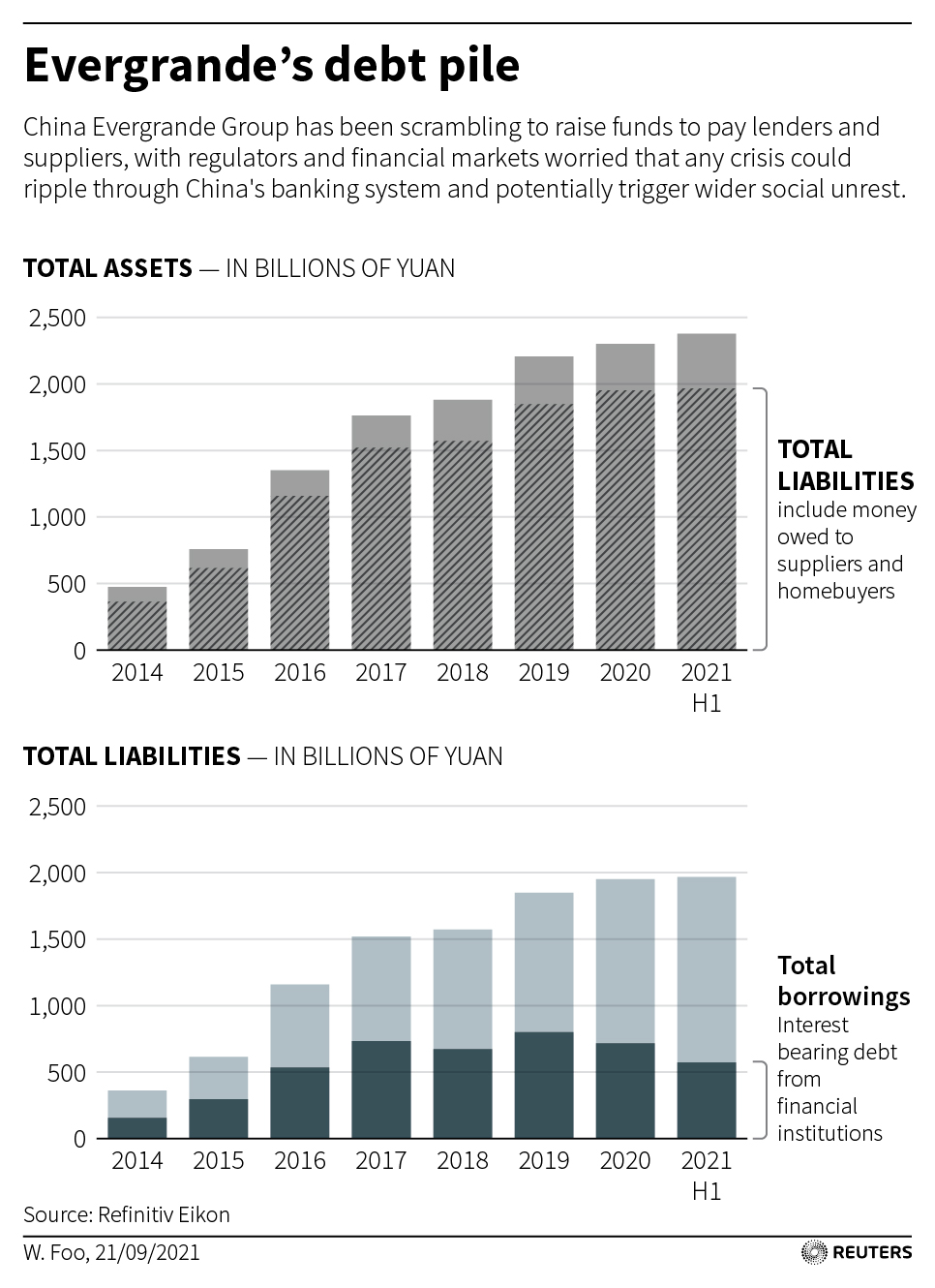

2️⃣ Evergrande’s $300 Billion Crisis

In 2021, China Evergrande Group defaulted on massive liabilities exceeding $300 billion — becoming one of the largest corporate debt crises in history.

Investor confidence collapsed.

3️⃣ Mortgage Boycotts

Homebuyers stopped paying mortgages on unfinished projects, exposing the weakness of China’s pre-sale model.

4️⃣ Demographic Decline

China’s population began shrinking, reducing long-term housing demand — a structural headwind rarely discussed during the boom.

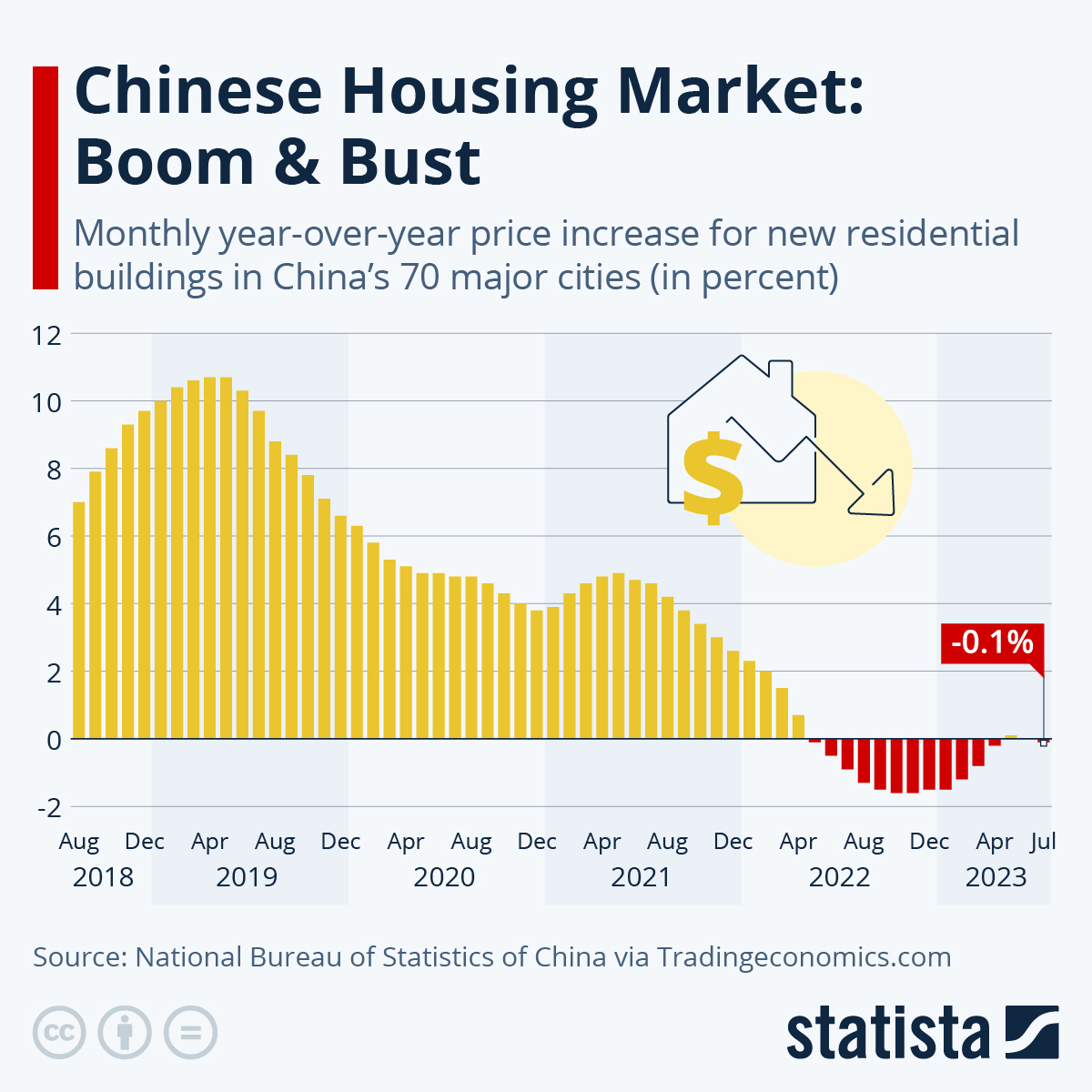

📊 Economic Impact on China

- Property prices declined across major cities

- Construction starts plunged

- Local government revenues from land sales collapsed

- Youth unemployment surged

- Bank balance sheets weakened

China’s GDP growth has slowed significantly compared to pre-pandemic averages.

Unlike the 2008 collapse of Lehman Brothers, China’s crisis remains largely contained domestically due to capital controls and state-dominated banking.

However, containment does not mean immunity.

🌍 Global Impact of China’s Real Estate Bust

China consumes massive amounts of:

- Iron ore

- Steel

- Copper

- Cement

The slowdown has hit commodity-exporting nations like Australia and Brazil.

Global implications include:

- Reduced global growth momentum

- Lower commodity prices

- Weak Asian market sentiment

- Pressure on emerging markets

📉 Is This a Bubble Burst or Structural Reset?

Many analysts now believe this is not a cyclical downturn but a structural deleveraging phase.

China is attempting to transition from:

🏗 Property-led growth

➡ Manufacturing, technology & domestic consumption

But such transitions take years — even decades.

Japan’s 1990 property collapse remains a historical parallel.

📊 Investor Risk Analysis

⚠ Key Risks

- Continued developer defaults

- Weak consumer confidence

- Banking sector stress

- Prolonged deflation

✅ Potential Opportunities

- Distressed asset acquisitions

- State-backed developer consolidation

- Selective equity recovery plays

- Commodity price stabilization cycles

Investors must differentiate between short-term volatility and long-term structural repositioning.

📌 Lessons for Indian & Global Investors

India’s property sector is structurally different:

- Lower household leverage

- Stronger end-user demand

- Regulatory oversight under RERA

- Demographic growth tailwinds

However, lessons include:

✔ Avoid excessive developer leverage

✔ Monitor pre-sale funding risks

✔ Watch speculative oversupply

✔ Diversify geographically

📈 Infographic: China Real Estate Crisis Snapshot (2026)

4

📌 Timeline Overview

2015–2019 → Peak property expansion

2020 → Three Red Lines policy introduced

2021 → Evergrande defaults

2022 → Mortgage boycotts spread

2023–2025 → Continued developer distress

2026 → Structural adjustment phase

🔮 China Property Market Forecast 2026–2030

Most economists expect:

- Stabilization rather than rapid recovery

- Gradual price correction

- Government-supported project completions

- Slower but more sustainable growth model

A sharp rebound appears unlikely without major fiscal stimulus.

🏁 Final Takeaway

China’s real estate bust is not merely a housing correction — it marks the end of an era of debt-driven expansion.

The long-term story now hinges on whether China can reinvent its growth engine beyond property.

For global investors, the message is clear:

Real estate bubbles built on leverage eventually correct — even in the world’s second-largest economy.